What is a bank card? 3+ information you need to know about bank cards

25/04/2025

Bank cards have become an indispensable part of modern life, especially when the cashless payment trend is booming. In this article, SeABank will provide all the information you need to know about bank cards, helping you better understand card types, costs, benefits, and how to choose the right card.

Note: The content in the article is compiled from general market information and does not solely represent SeABank's products and services.

1. What is a bank card?

Bank cards are payment instruments issued by banks, supporting customers in performing financial transactions without cash, such as: paying bills, withdrawing money, transferring money, and online shopping...

Bank cards help minimize financial risks by allowing customers to avoid carrying large amounts of cash. Additionally, with the security technology with advanced features such as data encryption and two-factor authentication, bank cards ensure maximum security in every transaction. Therefore, the use of bank cards is becoming increasingly popular and important in the digital age.

Bank cards are popular in the digital age.

Bank cards play an important role in optimizing financial transactions and managing personal spending:

Supports quick withdrawal: Users can easily make cash withdrawal transactions at ATMs nationwide.

Ensuring convenience in transfer: Customers perform simple operations with bank cards to transfer money domestically and internationally quickly and safely.

Promote non-cash payments: Instead of having to go to the store to pay cash, customers can use cards to pay bills, shop online and offline, conveniently, anytime, anywhere.

Manage finances effectively: Thanks to banking application integration, users can easily track spending, control accounts and plan personal finances scientifically.

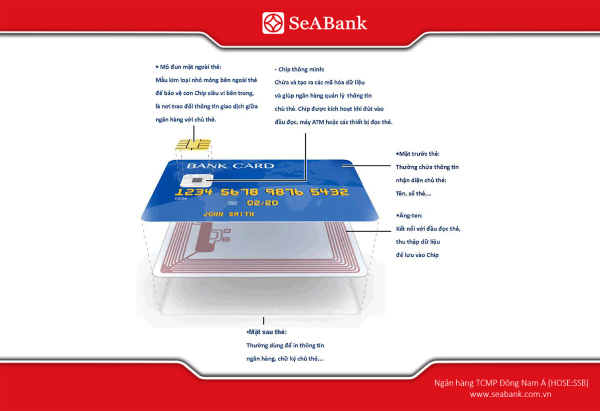

2. Bank card structure

A bank card is structured to include specific components to ensure convenience, identification, and safety in all transactions. Below is the basic structure of a bank card:

Size: According to ISO 7810 standards, bank cards have dimensions of 85.6 x 53.98mm.

Material: Cards are usually made from durable PVC; some high-end cards can be made from metal or recycled plastic.

Detailed structure of a bank card.

2.1. Front of card

The front of a bank card not only shows basic information but is also a factor that helps identify and ensure security for users. Below are the important elements on the front of the card.

Issuing bank name: Displays the bank logo and brand to help users easily identify.

Card number: A series of 16 - 19 digits used to identify the card. In there:

The first numbers represent the bank code (BIN - Bank Identification Number).

The remaining numbers are the cardholder's personal identification code.

Cardholder name: Embossed on the card, showing the legal owner.

Expiry Date: Represents the time the card is valid.

EMV Chip: A small microchip that enhances security and prevents data copying.

Card issuer logo: For example: Visa, Mastercard, JCB... represents the network using the card.

Bank card front SeABank.

2.2. Back of card

The back of the bank card contains important information to support transactions and ensure safety during use.

Magnetic Stripe: Stores basic card information to perform transactions.

Security code (CVV/CVC): Contains 3 digits, used for verification when paying online.

Signature area: This is where the cardholder signs to confirm ownership.

Bank information: Includes support hotline and official website.

Back of bank card.

In addition, the colors and patterns on bank cards are designed to have the unique characteristics of each bank or issuing organization. At the same time, some banks allow customers to choose their images to print on the card.

2. How many types of bank cards are there?

Bank cards today are very diverse, classified according to many different criteria to maximally meet the needs of customers in each financial field.

2.1 According to a financial source

Bank cards are classified based on financial sources, flexibly meeting customers' needs.

Prepaid card

Debit card

Credit card

Source of money

Use the amount the customer has previously loaded onto the card.

Excerpted directly from the Bank account linked to the card of customers.

The bank grants a credit limit, allowing customers to spend in advance and repay at the end of the monthly payment period.

Conditions for using the card

No bank account required, just add money to the card and you can use it.

Requires a bank account to link to the card.

Require proof of income and credit score to receive a monthly card limit.

Main function

Spend, shop, withdraw money.

Spend, transfer, and withdraw money.

Spend, pay online, accumulate points, pay in installments.

Usage limit

Equal to the amount loaded onto the card.

By account balance.

According to the credit limit granted by the bank.

Additional features

Do not have.

Domestic and international transactions.

Many incentives such as refunds, points, and discounts.

Debit card BRG Elite issued by SeABank.

2.2 According to territorial scope

Bank cards are classified by territory to help meet transaction needs from domestic to international, bringing convenience to users everywhere.

Domestic card

International card

Scope of use

For use only within Vietnam territory.

Used both domestically and internationally.

Issuing unit

Issued by domestic banks.

Issued by domestic banks in cooperation with international organizations such as Visa, Mastercard, JCB, UnionPay, or American Express.

Purpose

Payment and withdrawal domestically

Pay, shop, withdraw money globally at places that accept payment card systems (Visa, Mastercard systems...).

Usage costs

Low fees, no international transaction fees apply.

There are international transaction fees and foreign currency conversion fees.

SeA-Easy international credit card by NSeABank line.

2.3 According to card technology

With the development of technology, bank cards are increasingly equipped with advanced features.

Magnetic card

Chip card

Contactless chip card

Image

Identification signs

Black magnetic strip on the back of the card.

There is a yellow EMV chip on the front of the card.

There is a symbol of a signal tower (like a Wi-Fi signal) on the front or near the chip.

Technology

Magnetic strip to store information, use a card swiping machine.

EMV chip encrypts data, making transactions safer.

The EMV chip combines NFC technology to enable contactless payments.

Security

Low, susceptible to copying information from the magnetic strip.

High data encryption for each transaction, reducing the risk of fraud.

High, dynamic encryption, security similar to chip cards.

Utilities

Suitable for basic transactions such as withdrawals and domestic payments.

Use for both domestic and international transactions.

Payment is quick and convenient, reducing direct contact.

How to use

Swipe your card on the POS machine or withdraw money at the ATM.

Insert the card into the POS or ATM, and request the PIN code.

Tap the card near the NFC-enabled POS machine (no physical contact required).

Application

Traditional ATMs and POS machines.

POS Machine with NFC, ATM Machine, Traditional POS Machine.

POS Machine with NFC, ATM Machine, Traditional POS Machine.

SeABank's S24++ domestic contactless debit card is recognized thanks to bank and card organization logos, EMV chip, and easy-to-see contactless logo.

2.4 According to the card form

Bank cards include traditional physical cards and modern non-physical cards, meeting a variety of users' financial transaction needs.

Physical card

Non-physical card

Form

Hard card, standard size

There is no physical card, it only exists as a card number or in the app

Uses

Payment at POS, ATM withdrawal

Pay online, via application, or e-wallet

Confidentiality

High with EMV chip or PIN code

High with OTP code, in-app encryption

Utilities

Can be used for both offline and online transactions

Focus on online transactions, no need to carry a physical card

Suitable subject

People who regularly trade directly

Users shop online or prioritize cashless payments

SeABank currently issues many types of physical bank cards, serving a diverse customer base.

SeABank provides a variety of bank cards, from high-end international credit cards such as SeALady Cashback, SeA-Easy, Visa Platinum to domestic and international debit cards such as SeABank S24++. The cards are designed with many benefits such as cashback, annual fee waiver, partner discounts and high-value insurance...

3. Instructions for opening a card at SeAbank

To help customers easily own a suitable bank card, below are detailed instructions on conditions, processes, and important notes when opening a card at SeABank.

3.1. Conditions for opening a card at SeABank

According to card card-making regulations bank, updated in 2023, stipulates:

3.1.1 For primary cardholders who are individuals

People from 15 to 18 years of age or older with full civil act capacity according to the provisions of law can make debit cards, credit cards, and prepaid cards.

3.1.2 For cardholders who are organizations and businesses

Organizations eligible to open payment accounts may use debit cards.

Organizations that are legal entities established and operating legally by Vietnamese law may use credit cards and prepaid identification cards.

The cardholder is an organization that authorizes in writing an individual to use that organization's card or allows an individual to use a supplementary card according to regulations.

3.1.3 Conditions for making a bank card for supplementary cardholders

People from 15 to 18 years of age or older with full civil act capacity according to the provisions of law can make debit cards, credit cards, and prepaid cards in the form of supplementary cards according to the specific instructions of the main cardholder.

A person from full 6 years old to under 15 years old who has not lost or limited his or her civil act capacity must have his/her legal representative agree in writing to use the card as a debit card or prepaid card in the form of a supplementary card according to the specific instructions of the main cardholder.

3.2. Card opening process at SeABank

To make card opening procedures at SeABank quick and convenient, customers need to follow these steps:

Step 1: Prepare Documents

To open a bank card at SeABank, you need to prepare the following basic documents:

Personal documents: ID card/CCCD or valid passport.

Additional documents (if necessary): Depending on the card type, customers may need additional documents proving income or collateral.

Card opening registration form: Customers can fill in directly at the transaction counter or on SeABank's online system.

Step 2: Register to open a card

After completing the application, customers can choose to register to open a card at the transaction counter or online.

At the transaction counter:

Go to the nearest SeABank branch for support.

Fill out the card opening registration form and apply.

Enter the online card opening registration information according to the instructions.

Bank staff will contact you to confirm information and complete the application.

Step 3: Review and issue the card

After receiving the application, SeABank will review it to ensure the information is accurate and eligible to issue the card.

Review time: Normally, applications are processed within 3-5 working days.

Card issuance: After the application is approved, the card will be issued, and the bank will notify the customer via SMS or email.

Step 4: Receive and activate the card

To use the card, customers need to receive the card and activate it according to instructions from SeABank.

Get a card:

At the SeABank branch where you registered to open the card.

Or receive by mail if requested.

Activate card:

Call SeABank's customer service hotline to activate.

Or activate directly at SeABank ATMs by entering the PIN code for the first time.

The fast card opening process is quick and convenient at SeABank.

3.3. Note when opening a card at SeABank

To make the card opening process at SeABank go smoothly and ensure the best experience, customers need to note the following important points:

Fees and interest rates: Customers should carefully learn about related fees such as annual fees, interest rates, and transaction fees for each card type, according to their financial needs.

Endow: When using SeABank cards, customers can receive incentives from SeABank's customer care programs, such as refunds, discounts when shopping, or annual fee waivers for specific card lines.

Security: This is an important note. SeABank advises customers to:

Protect card information, especially PIN and transaction details.

Do not share card information with anyone, especially when transacting online.

Regularly check transaction history to promptly detect unusual transactions.

Determine sufficient usage limit - for credit cards: In addition to appraisal from the bank, customers need to clearly determine the spending or withdrawal limit for each type of card to use it effectively and avoid exceeding the prescribed limit.

Choose the appropriate card type: Depending on personal needs (domestic spending, international spending, or online payment), customers should choose the appropriate card line such as debit card, credit card or prepaid card.

4. Answers to frequently asked questions

Question 1: How long does it take to receive the card after registering at SeABank?

After completing the registration procedure, customers usually receive the card within 5-7 working days. If you need to use your card sooner, SeABank provides a quick card issuance service, helping you shorten the time to receive your card as much as possible.

Customers, please contact the nearest branch directly for detailed service support.

Question 2: How to activate the SeABank bank card?

You can activate the card by calling SeABank's customer service switchboard or activating it directly at the bank's ATM. Make sure you have received the PIN code provided by your bank to complete the activation process safely and quickly. In case you need additional support, SeABank staff are always ready to guide you.

Question 3: What special offers does the SeABank card have?

Each type of SeABank card is designed to benefit customers with attractive incentives, including:

For debit cards

Unlimited cash back when spending on online shopping or payment transactions.

Discount up to 70% at SeABank partners.

Enjoy attractive interest rates on the account balance linked to the card.

For credit cards (credit cards)

Free first-year annual fee for many premium card lines.

Offering high-value insurance, up to 10 billion VND, for customers using special credit cards (Visa Signature, BRG Elite).

Cash back offers from 1% to 10% when shopping, paying bills, or booking travel tickets.

Free 24/7 healthcare benefits for premium cardholders.

Bank cards today play an important role in optimizing financial management and meeting customers' payment needs. With a variety of products and outstanding utilities, SeABank offers effective, safe and modern financial solutions. Please consider and choose the appropriate bank card product to experience the best preferential services from SeABank.

Southeast Asia Commercial Joint Stock Bank SeABank

Address: BRG Building, 198 Tran Quang Khai, Ly Thai To Ward, Hoan Kiem District, Hanoi